The classic asset-allocation rule of thumb — 100 minus your age in stocks, the rest in bonds — has been around since the 1950s. It's tidy. It's memorable. It's also outdated for several reasons that matter.

People live longer. Bonds yield less than they used to. Behavioral finance has revealed how badly investors react to volatility. And the same 60-year-old who needed a conservative allocation in 1960 might have a 25-year retirement horizon today rather than 15. The rule of thumb hasn't kept up.

This isn't an argument for complicated allocations. Simple is still better. But here's a more honest framework, by life stage.

The Three Variables That Actually Matter

Before any age-specific advice, the three things that should drive your allocation:

1. Time horizon

When will you actually need to spend the money? Not retire — spend. A 65-year-old retiree might still have a 25-year time horizon for the long-tail portion of their portfolio. A 30-year-old saving for a house in 4 years has a much shorter horizon for that money than for retirement money.

Many investors collapse "retirement age" into "time horizon" and end up too conservative for the back half of retirement, where money still needs to grow to last 30 years.

2. Risk tolerance (real, not imagined)

How would you actually behave if your portfolio dropped 35% in three months? Two answers count:

- The honest answer: based on what you actually did in 2008, March 2020, or 2022.

- The honest answer if you've never been through a bear market: assume your imagined tolerance is roughly 1.5× your actual tolerance. Most first-time bear market investors discover they hate it more than they thought.

The point of identifying your real risk tolerance is that the worst time to discover you can't tolerate volatility is during a bear market. Better to under-allocate to stocks and stay invested than over-allocate and panic-sell.

3. Human capital

If your career income is stable and predictable (tenured professor, federal employee, doctor in a stable practice), your "human capital" already acts like a bond — a reliable income stream you can count on. You can hold more equity in the financial portfolio because the rest of your wealth has bond-like properties.

If your income is volatile (commission sales, freelance, business owner, equity-heavy compensation), your human capital is more equity-like. You may want a more conservative financial portfolio to balance.

In Your 20s: Front-Load the Risk

Investing in your 20s is mostly about getting started and not doing anything stupid. Time horizon is 40+ years. Volatility is irrelevant in any single year because there are decades to recover.

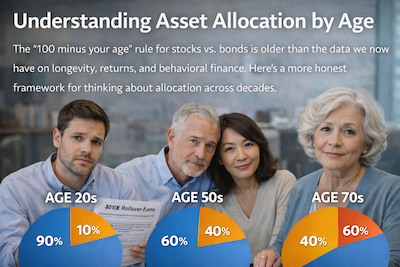

Reasonable allocation: 90–100% equities, 0–10% bonds.

Within equities: Heavy global diversification — roughly 60–70% US, 30–40% international. A 5–10% small-cap or emerging-markets tilt is reasonable but not required.

What to actually do:

- Capture every dollar of your employer 401(k) match. This is a 50–100% guaranteed return and the highest-priority investing move at any age.

- Open a Roth IRA if your income is below the limit. At a low tax bracket today, paying tax now and getting tax-free growth forever is a great trade.

- Automate everything. Set the contribution and forget. The biggest threat to long-term returns at your age is interrupting the contribution stream during life events.

- Index funds, not stock-picking. Building expertise in individual security selection is a multi-decade project, and most people who try it underperform a 3-fund index portfolio over time.

- Don't overthink the bond allocation. A 25-year-old with 100% equities and a 25-year-old with 90/10 will end up in roughly the same place over 40 years.

The biggest mistake at this age isn't the allocation itself — it's not investing at all, or pulling money out for short-term goals.

In Your 30s: Build the Habit

Time horizon is still 30+ years. Family obligations may be picking up. Career income is rising. The right allocation is still equity-heavy but the behavior matters more than the percentage.

Reasonable allocation: 85–95% equities, 5–15% bonds.

What to actually do:

- Increase contributions as income rises. A 25-year-old saving 10% becomes a 35-year-old saving 15%, becomes a 45-year-old saving 20%. The ramp is more important than any allocation tweak.

- Diversify account types. Build up a taxable brokerage alongside retirement accounts. Future flexibility (early retirement, sabbaticals, opportunistic moves) requires money you can access without penalty.

- Don't panic-shift to bonds during your first bear market. This is the most common allocation mistake at this stage. You have 30+ more years; recovery is essentially guaranteed if you stay invested.

- Resist concentrated stock positions. If you have RSUs or ESPP from your employer, sell them periodically rather than letting them accumulate. Single-stock concentration plus career exposure to the same company is too much risk.

In Your 40s: Catch Up If You Need To

Mid-career is when the gap between "saving aggressively enough" and "barely saving" becomes visible. If you started early, you're cruising. If you didn't, you have 20–25 years of compounding left to make it work — challenging but doable.

Reasonable allocation: 75–90% equities, 10–25% bonds.

What to actually do:

- Maximize tax-advantaged contributions. 401(k) limits, IRA limits, HSA if available. Dollar-for-dollar tax savings here matter more than allocation tweaks.

- Audit and consolidate. If you've changed jobs a few times, you may have 401(k)s scattered across former employers. Roll them into a single Traditional IRA for cleaner management.

- Add international and small-cap diversification deliberately. US-dominated portfolios have outperformed for the last decade; don't extrapolate. Hold roughly 30–40% international.

- Increase savings rate, not portfolio risk. If your retirement projections are short, the answer is "save more," not "take more risk." Adding equity to compensate for under-saving is taking on tail risk that may not pay off in time.

In Your 50s: Glide Path Begins

Retirement is in sight but not imminent. The portfolio is (hopefully) at its largest. Sequence-of-returns risk starts to matter — a 30% drop in your last three working years can permanently delay retirement.

Reasonable allocation: 60–80% equities, 20–40% bonds.

What to actually do:

- Make catch-up contributions. At 50+, the IRS allows higher 401(k) contributions ($30,500 vs. $23,000 in 2024) and IRA contributions ($8,000 vs. $7,000). Use them.

- Begin de-risking, but not aggressively. A 30% drop two years before retirement hurts; a 30% drop in cash 30 years into retirement (because inflation ate it) hurts equally. Stay equity-heavy enough to keep growing.

- Audit fees seriously. A 1.5% AUM fee compounded over the next 25–30 years costs you 25–30% of your terminal wealth. If your advisor is expensive and not adding tax-planning value, switch.

- Run a real retirement projection. Not a back-of-envelope. A Monte Carlo simulation through a CFP or quality planning software (eMoney, MoneyGuide, RightCapital) will tell you whether you're on track and what to adjust.

- Plan the gap years. If you might retire at 60–62 but won't take Social Security until 67–70, you have a 5–10 year window where Roth conversions are unusually valuable. Start thinking about this now.

In Your 60s: Pre-Retirement and Early Retirement

The most consequential allocation period of your life. Sequence-of-returns risk peaks here. The mistake of being too conservative is symmetric with the mistake of being too aggressive.

Reasonable allocation: 50–70% equities, 30–50% bonds (with 1–2 years of expenses in cash separately).

What to actually do:

- Build a cash bucket. 1–2 years of expenses in high-yield savings or money market funds, separate from the bond allocation. The job of cash is to insulate you from selling stocks during a downturn.

- Optimize Social Security claiming. For most people, delaying to age 70 is the highest-leverage move available. A delayed benefit is essentially a guaranteed annuity that grows 8% per year, inflation-protected, and continues for life.

- Roth conversions in low-income years. As covered in our Roth conversion guide, the gap years between retirement and required distributions are uniquely good for converting at favorable brackets.

- Plan for healthcare bridge. If retiring before 65, the cost of health insurance until Medicare starts is often the single largest expense. Build it into your projections explicitly.

- Don't fully de-risk to cash. A 65-year-old retiring with 100% in cash and bonds may have a 25-year retirement during which inflation cuts purchasing power dramatically. Keep growth assets working.

In Retirement: Different Math

Once you're spending from the portfolio rather than adding to it, the framework changes. The question isn't "how do I maximize long-term growth" — it's "how do I sustain spending across 25+ years without running out of money."

Reasonable allocation: 40–60% equities, 40–60% bonds, with 1–2 years of cash. Adjust based on Social Security and pension coverage.

If your guaranteed income (Social Security, pension, annuity) covers 70%+ of your expenses, you can run a more aggressive portfolio because the residual you're managing isn't your survival money.

If your portfolio funds most of your living expenses, you'll want a more conservative allocation with more reliable cash flow, even at the cost of long-term growth.

The bucket strategy (covered in our bucket-strategy guide) is one common framework here.

Glide Paths vs. Static Allocation

A glide path is a programmed shift from equity to bonds over time — typically built into target-date funds. A 2055 target-date fund holds ~90% equities today; a 2025 fund holds ~50%. The fund automatically de-risks as the target date approaches.

For most people, target-date funds are a perfectly fine all-in-one solution. They handle allocation and rebalancing automatically; you don't have to think about it.

The trade-offs:

- Less control. You can't hold a different bond duration or international tilt than the fund manager chose.

- Slightly higher expense ratios than a self-managed three-fund portfolio (typically 0.10–0.15% vs. 0.05% for a custom portfolio).

- One-size-fits-most. A 2050 fund treats every investor with that retirement target identically, regardless of pension coverage, risk tolerance, or other assets.

For investors with simple situations who want to "set it and forget it," a target-date fund is reasonable. For investors with more nuanced situations (significant pension coverage, large taxable brokerage, business interests, multi-state retirement plans), a custom allocation typically beats the off-the-shelf product.

Rebalancing

Whatever allocation you pick, your portfolio drifts away from it over time as different asset classes perform differently. Rebalancing brings it back to target.

The two common approaches:

- Calendar-based: Rebalance once per year, regardless of how far off target you've drifted.

- Threshold-based: Rebalance when any allocation drifts by 5% or more from target.

For most investors, annual rebalancing is sufficient and behaviorally easier. Rebalancing too frequently (quarterly or monthly) tends to incur trading costs without meaningfully improving returns.

For taxable accounts, prefer rebalancing through new contributions (direct new money to the under-weight asset class) rather than selling appreciated positions, which triggers capital gains.

The Bottom Line

The "100 minus your age" rule is too simple. A modern allocation framework considers time horizon, risk tolerance (real, not imagined), human capital, and the specific challenges of the life stage you're in.

For most people the practical answer is somewhere between target-date funds (simplest) and a 3- or 4-fund index portfolio (most flexible). The exact percentages matter less than:

- Whether you contribute consistently

- Whether you stay invested through downturns

- Whether your fees stay low

- Whether you adjust thoughtfully as your situation changes

If you'd like a portfolio strategy designed for your specific life stage and risk tolerance, our directory lists fiduciary advisors who specialize in investment management across every state. Verify any advisor on FINRA BrokerCheck before you commit.